Decree 837: The Framework Is Written. Here's Where You Want to Be

China's first comprehensive outbound-investment framework supervises deals across their whole life, not just at entry. Three Southeast Asia investment types align with its grain.

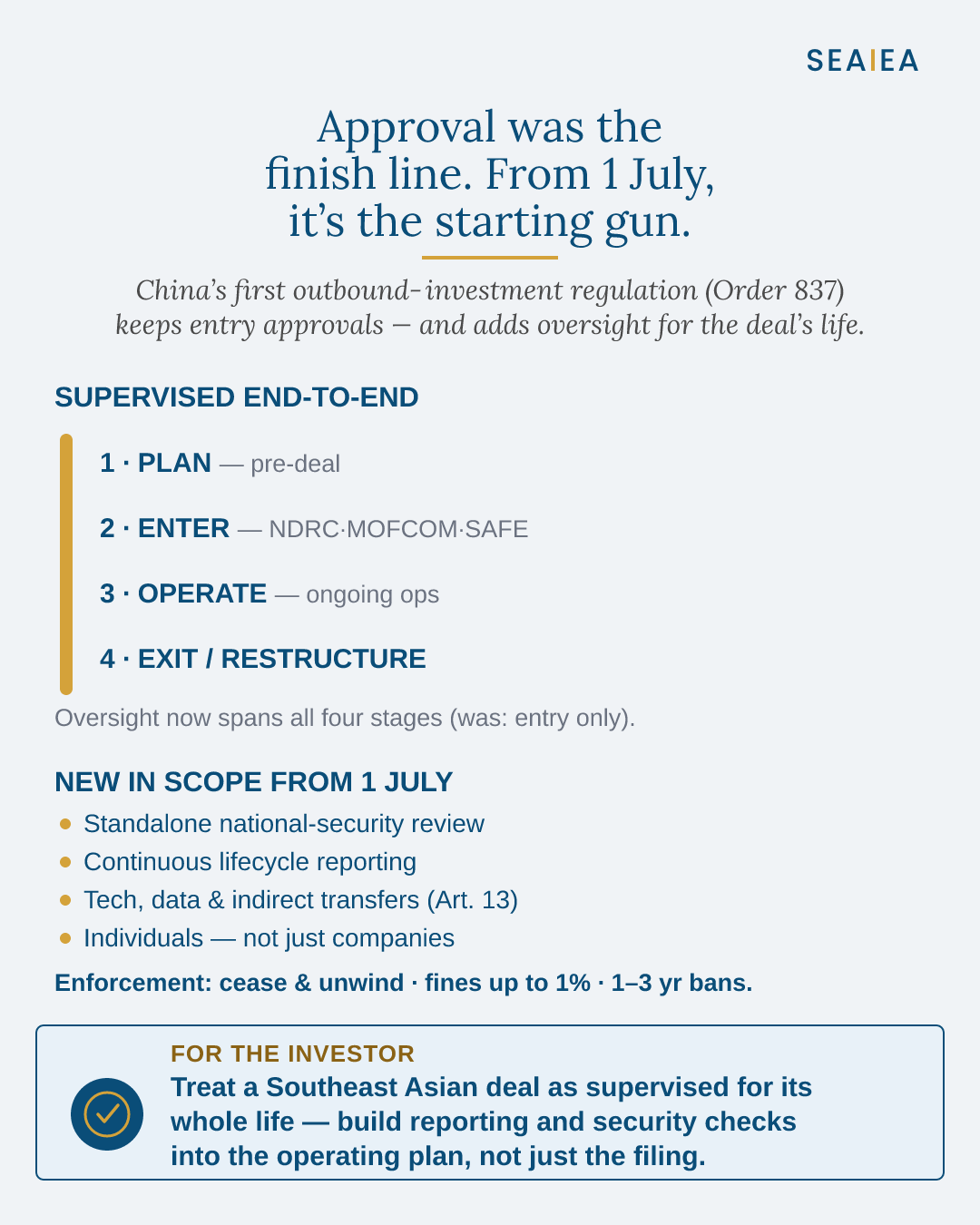

Everyone in Chinese investment circles is talking about State Council Decree No. 837. Signed May 5, published June 1, taking effect July 1 — it is China's first comprehensive statutory framework for outbound investment: 34 articles covering the full lifecycle of overseas expansion, from pre-investment filing and security review through ongoing compliance and enforcement, replacing a patchwork of ministerial rules accumulated over two decades.

It arrives as the third piece of a deliberate trilogy. Decree 834, issued in March, addressed industrial and supply-chain security. Decree 835, issued in April, established China's framework for countering improper foreign extraterritorial jurisdiction. Decree 837 completes the sequence. Together they follow a clear internal logic: build resilient supply chains, defend them against external pressure, then extend them on a governed basis.

The context is China's remarkable overseas footprint. Outbound direct investment stock reached $3.14 trillion at the end of 2024, spread across more than 50,000 Chinese-invested enterprises in 190 countries. Until now, this vast system operated under overlapping and inconsistent ministerial rules. Decree 837 replaces that patchwork with a single framework everyone can understand and follow.

China remains open for overseas expansion — that direction will not change. The regulation does not tell firms where to invest or whether to invest. Articles 4 and 5 explicitly reaffirm investors' commercial autonomy and their right to bear their own risks and returns. What Decree 837 does is define the institutional framework within which that expansion now takes place, and set the outer boundaries clearly so no one is guessing.

It also does something worth paying attention to. Articles 6 through 9 mandate a comprehensive overseas service system: diplomatic support, legal services, financial and tax guidance, customs coordination, logistics, and political risk insurance — all backed by the state and increasingly anchored in Chinese-operated professional services. SASAC established a dedicated Bureau of Overseas Foreign Investment Administration in April to centralise support and coordination for SOE international projects. This is not new in principle: it mirrors what German, Japanese, and American multinationals have received from their home governments for decades. China is now building its own equivalent. Chinese firms heading abroad after July 1 will work within a support system they understand and can rely on.

In a more complex global investment environment, some deal structures that worked well in earlier years require more careful navigation. The new framework makes clear where the grain of the wood runs.

For investors heading to Southeast Asia, three types of investment align most cleanly with this framework. The first is upstream resource and processing that feeds directly into Chinese supply chains. Indonesia's nickel sector is the benchmark: Chinese firms control approximately 75% of Indonesia's nickel refining capacity, vertically integrated from ore through to battery-precursor materials. The Indonesia Morowali Industrial Park alone has absorbed roughly $8 billion in cumulative investment; a CATL-led integrated battery project spanning mining to recycling added a further $6 billion in 2025. Indonesia is on course to supply the majority of the world's nickel within the decade. Output flows into Chinese EV battery manufacturers; the supply chain runs back to China. Decrees 834 and 837 together were built to support and protect exactly this structure.

The second is Chinese brands expanding into Southeast Asian markets. The region is heading toward being the world's fourth-largest economy by 2030, with nearly 700 million consumers and Vietnam growing at 7–8% annually. Chinese brands are already moving at scale: Mixue has built a significant franchise footprint in Vietnam, BYD opened a 150,000-unit assembly plant in Thailand in July 2024, and Chinese EV dealership networks are expanding across Vietnam, Indonesia, and Malaysia. The technology is Chinese, the brand is Chinese, the supply chain runs back to China. Regulatory complexity is minimal.

The third is manufacturing anchored to Chinese-led regional supply chains rather than oriented toward Western export markets — the distinction matters under the new framework. Malaysia illustrates the emerging opportunity: roughly 33 semiconductor projects worth approximately $20 billion are active across the country, and 42 data-centre projects worth some 164 billion ringgit have been approved in Johor. Regional digital and industrial infrastructure, plugged into Chinese-anchored technology ecosystems.

One provision worth understanding across all three categories is Article 13, which clarifies that overseas investment cannot serve as a channel for technology transfer outside approved pathways — including through personnel secondment, training of joint-venture partners, or remote technical guidance. For the investment types above, this creates minimal friction: the technology stays within the Chinese system. For investments involving deep technical integration with non-Chinese partners, careful structural planning from the outset will be time well spent.

The game has changed, but it can still be played. Invest in what serves Southeast Asia's domestic market, or in what flows back into China's industrial and consumer networks. Keep the technology, the brand, and the supply chain within the Chinese ecosystem. Do this, and you will have behind you exactly the institutional support this framework was designed to provide.

- National investment boards; government announcements; SEAIEA analysis

Get The Weekly Read every week

ASEAN investment commentary, free to subscribers.